Get free quotes from verified manufacturers and suppliers

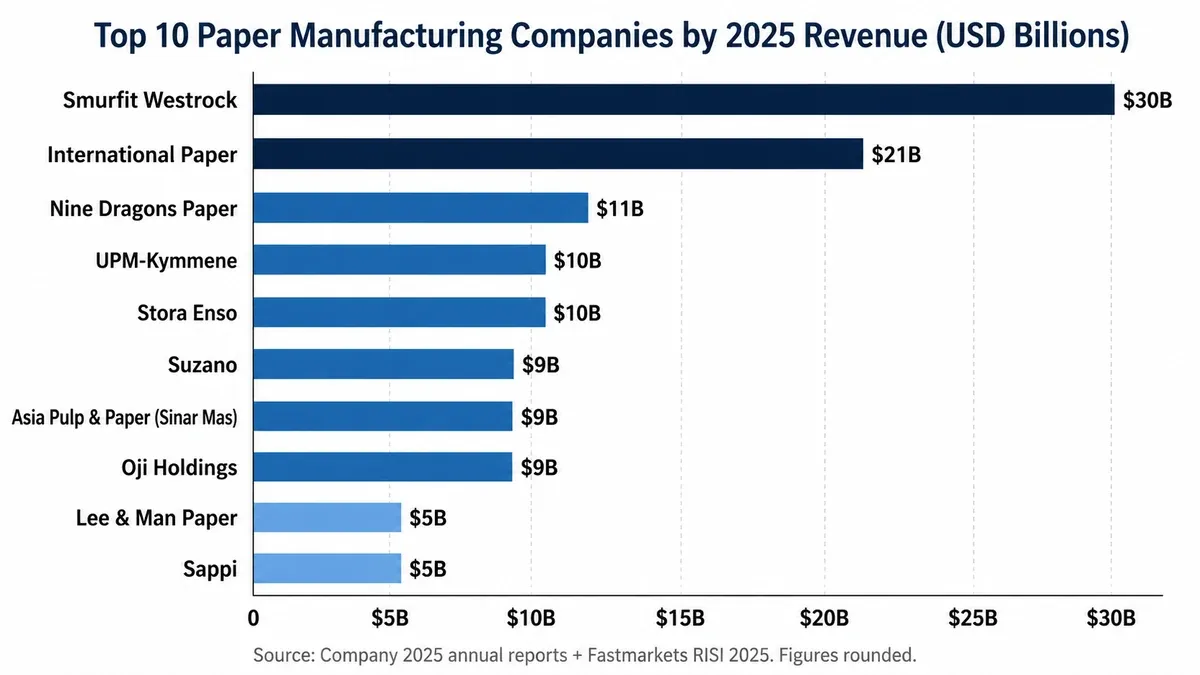

Quick Answer: Smurfit Westrock now leads global paper manufacturing after its July 2024 merger, with about $30 billion in revenue. International Paper holds the #2 position near $21 billion, followed by Nine Dragons Paper (~$11 billion), UPM-Kymmene, and Stora Enso. Together, the top 10 producers run more than 600 mills across 50+ countries and churn out over 110 million tonnes of paper and paperboard a year (FAO Forestry Database 2025 plus company annual reports).

Last updated: 13 May 2026 by the World Paper Mill editorial team. Sources: company 2025 annual reports (published Q1 2026), Q1 2026 quarterly filings, SEC and HKEX filings, Fastmarkets RISI 2025 industry data, AF&PA Q1 2026 outlook, and CEPI preliminary statistics February 2026.

Top 10 Largest Paper Manufacturing Companies 2025-2026

A handful of integrated producers control most of the global paper industry. The landscape shifted dramatically in 2024 when WestRock and Smurfit Kappa merged to form Smurfit Westrock, displacing International Paper from the #1 spot it had held for years. Chinese producers Nine Dragons and Lee & Man have climbed steadily through vertical integration and aggressive capacity expansion. Brazil's Suzano remains the world's largest hardwood pulp exporter on the back of its short-rotation eucalyptus plantations.

Revenue figures combine 2025 full-year audited reports with Q1 2026 quarterly results where available, rounded. INR conversions use roughly ₹83 per USD (RBI 2026 reference). Production capacity includes paper, paperboard, and pulp combined. Sources: company 2024 annual reports, SEC filings, HKEX disclosures, Fastmarkets RISI 2025.

Note on figures: Revenue and production capacity numbers shown are 2025 full-year estimates with Q1 2026 trajectory signals, rounded for comparability. Specific values change with each quarterly earnings release, currency fluctuation, and merger / divestiture activity. Asia Pulp & Paper figures are aggregated industry estimates since the company is privately held. Always validate against current company 10-K, 20-F, or HKEX disclosures before making investment or partnership decisions.

Top 10 Paper Manufacturing Companies by 2025 Revenue: Smurfit Westrock leads at $30 billion (post-2024 merger), nearly $9 billion ahead of #2 International Paper. Source: Company 2025 annual reports and Fastmarkets RISI 2025.

A Closer Look at Each Company

#1. Smurfit Westrock: The New Global Heavyweight

Smurfit Westrock did not exist as a single entity two years ago. The July 2024 combination of Atlanta-based WestRock (founded 1936) with Dublin-based Smurfit Kappa (founded 1934) created a packaging giant overnight, with combined revenue near $30 billion and around 100,000 employees across 40+ countries.

CEO: Tony Smurfit

Stock: NYSE: SW, LSE: SWR (dual listing)

Production capacity: ~25 million tonnes/year of paper-based packaging

Sustainability: FSC and PEFC chain-of-custody certified, net-zero target by 2050

The strategic logic behind the merger was straightforward. Smurfit Kappa brought European leadership; WestRock contributed North American containerboard scale. Both legacy companies already had Latin American operations that could be consolidated. The result is a producer that outflanks International Paper in geographic reach and packaging share.

#2. International Paper Company: The 127-Year-Old Veteran

Few industrial companies have survived as long as International Paper. Founded in 1898 and headquartered in Memphis, IP weathered the Great Depression, two World Wars, and the structural decline of graphic paper. The company now generates 2025 revenue around $22 billion and has roughly 38,000 employees.

IP is positioned for a major change in 2026. The pending acquisition of UK-based DS Smith, valued near $9.9 billion when announced in late 2024, will push combined revenue past $25 billion and considerably strengthen IP's European packaging footprint. CEO Andrew Silvernail (since 2024) has signaled a portfolio simplification under way.

Production capacity sits around 17 million tonnes per year across 24 manufacturing facilities in 13 countries. The product mix tilts heavily toward packaging (about 70%), with the rest in pulp (including fluff pulp for tissue and hygiene) and specialty grades.

#3. Nine Dragons Paper Holdings Limited

Few companies in any industry have grown as fast as Nine Dragons. Founded in 1995 by Cheung Yan (one of the world's wealthiest self-made women), the Hong Kong-listed producer has scaled to about 20 million tonnes per year of containerboard from recycled fiber, making it the largest containerboard producer globally per Fastmarkets RISI 2025.

Revenue runs around $12 billion (HK$90+ billion) in 2025 and the company employs roughly 38,000 people across nine production bases in China and one in Vietnam. The product mix is essentially pure recycled-fiber packaging, with closed-loop water systems and a sourcing operation that spans domestic Chinese OCC plus imports.

UPM is a bet on the post-paper future of forestry. Formed in 1996 through the merger of three Finnish forestry companies, UPM has steadily diversified beyond traditional paper into six business areas: Communication Papers, Specialty Papers, Biorefining (pulp), Raflatac (labels), Plywood, Biofuels, and Energy. The Leuna biorefinery in Germany, ramping production through 2025-2026, produces renewable functional fillers and chemicals from wood biomass.

Headquartered in Helsinki and led by Massimo Reynaudo (since 2024), UPM posted around €9.6 billion / $10.3 billion in 2025 revenue, with capacity near 10 million tonnes/year across 16 mills in Europe, North America, China, and Uruguay. Roughly 17,000 employees. Both FSC and PEFC certified.

#5. Stora Enso Oyj: One of the World's oldest continuous businesses

Stora Enso's lineage traces back to 1288, making the company's founding ironworks one of the oldest continuous business operations on the planet. The modern Stora Enso was formed in 1998 by merging Swedish Stora Kopparberg and Finnish Enso Oyj. Today the company is headquartered in Helsinki, led by Hans Sohlstrom (since 2024), and listed on both Helsinki (HEL: STERV) and Stockholm exchanges.

The strategic direction is clear: pivot hard from graphic paper into packaging, biomaterials, and bio-based chemicals. The 2024-2025 partnership with Sappi to consolidate European graphic paper capacity reflects that thesis. Revenue is around €8.7 billion / $9.7 billion in 2025; production capacity near 9 million tonnes/year across 50+ units in Europe, China, and Latin America. Around 21,000 employees globally. Carbon-neutral operations target: 2030.

#6. Suzano S.A.: The Eucalyptus Advantage

Suzano dominates global bleached hardwood pulp export, and the company's structural advantage is rooted in geography. Brazilian eucalyptus plantations rotate in 7 years; northern hemisphere boreal softwood takes 25 to 40 years. That difference in rotation cycle gives Suzano a cost edge that competitors cannot match without similar plantation access.

Formed in its modern shape in 2019 through the merger of Suzano and Fibria (the original Suzano company dates to 1924), the producer is headquartered in Sao Paulo. CEO Joao Alberto Fernandez has led since 2024. Stock: NYSE: SUZ and B3: SUZB3.

2025 revenue ran around $9.5 billion, primarily from pulp exports rather than finished paper. Production capacity sits near 12 million tonnes/year of bleached eucalyptus kraft (BEK) plus paper grades, across 11 major industrial units in Brazil. About 40,000 employees. FSC and PEFC certified with significant Cerrado biome conservation programs.

#7. Asia Pulp & Paper (Sinar Mas Group)

APP is the major exception to public disclosure in this list. Held within Indonesia's privately-owned Sinar Mas Group (controlled by the Eka Tjipta Widjaja family), the company does not publish consolidated audited financials. Industry estimates put 2025 revenue at $9.5 billion-plus, with around 19 million tonnes/year of combined paper, paperboard, and pulp capacity. The workforce across the group is near 70,000.

APP runs nine paper and pulp mills in Indonesia plus China operations. The product mix spans tissue, packaging, fine paper, and acacia pulp. Sustainability has been an area of evolution: APP has expanded its FSC and PEFC certification footprint substantially over the past decade, though historical deforestation criticism still attaches to the company.

#8. Oji Holdings Corporation: Japan's paper giant

Oji traces its modern foundation to 1873, making it one of the older operating paper companies in Asia. Headquartered in Tokyo and led by Hiroyuki Isono, Oji is Japan's largest paper producer and operates a remarkably diverse product mix: about 30% packaging, 25% functional paper, 20% household tissue, 15% printing and publication, and 10% specialty grades.

2025 revenue ran around ¥1.55 trillion / $10.3 billion with capacity near 10 million tonnes/year across 40+ production facilities in Japan, Southeast Asia, Australia, and New Zealand. Around 37,000 employees globally. The company has invested heavily in overseas plantation forests and pulp mills to secure fiber supply as domestic Japanese demand for graphic paper declines.

#9. Lee & Man Paper Manufacturing

Lee & Man is China's second-largest paper company after Nine Dragons. Founded in 1994 and chaired by Lee Man Bun, the producer is vertically integrated from recycled-fiber pulping through finished tissue and packaging products. HQ in Hong Kong with main operations in Dongguan and Chongqing (China) plus Vietnam.

2025 revenue: ~HK$38 billion / $4.9 billion. Capacity: ~10 million tonnes/year. Around 10,000 employees. Product mix runs roughly 70% containerboard, 20% tissue, 10% specialty kraft. Closed-loop water systems and recycled-fiber-heavy sourcing characterize the operation.

#10. Sappi Limited: The Dissolving Pulp Leader

Sappi has reinvented itself. Founded in 1936 in South Africa, the company is now the global leader in dissolving pulp (specialty cellulose) for textile manufacturing, supplying the viscose, lyocell, and modal fiber industry. Headquartered in Johannesburg, listed on JSE: SAP and NYSE: SPP (sponsored ADR), led by CEO Steve Binnie.

The product mix is genuinely unusual: about 40% coated graphic paper, 30% specialty cellulose (dissolving pulp), 20% packaging, and 10% specialty. 2025 revenue ran near $5.2 billion with capacity around 5 million tonnes/year across 17 production facilities in 9 countries. About 12,000 employees. The 2024-2025 partnership with Stora Enso consolidates European graphic paper capacity to manage that segment's structural decline.

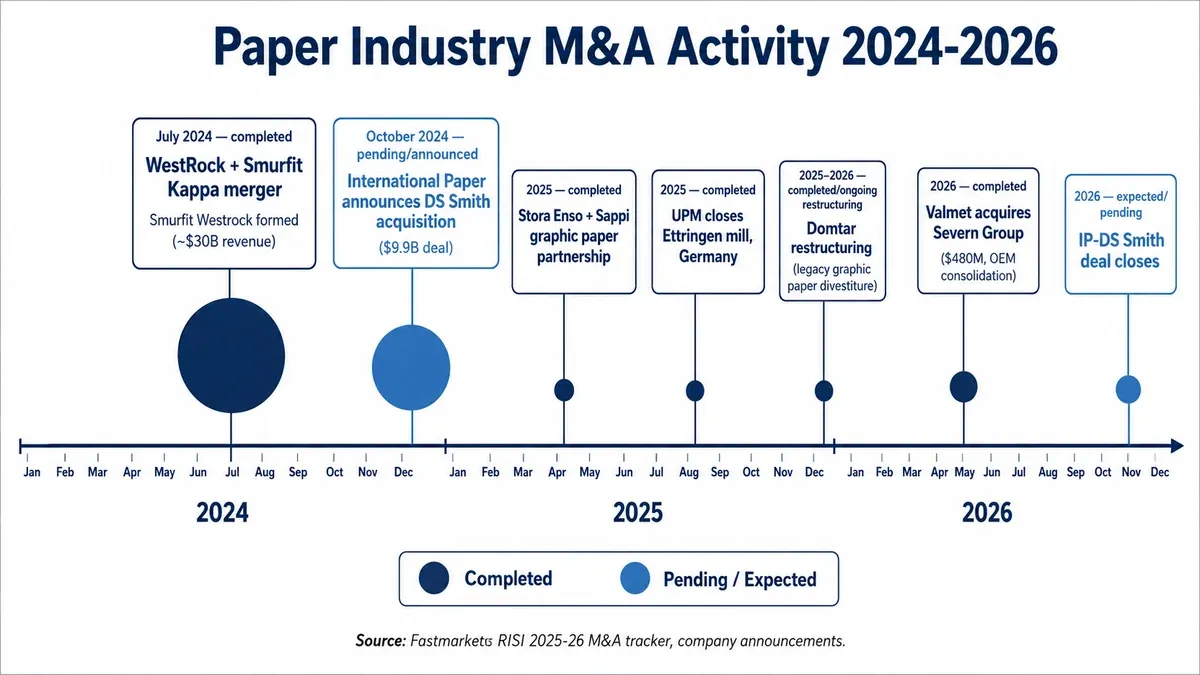

M&A Activity 2024-2026

Paper-industry consolidation has accelerated through 2024-2026 as graphic paper declines, energy costs bite, and Chinese exports pressure margins. Key transactions to note:

Paper Industry M&A Activity 2024-2026: The Smurfit Westrock merger in July 2024 anchors the consolidation wave reshaping global paper packaging. Source: Fastmarkets RISI 2025-26 M&A tracker, company announcements.

July 2024: WestRock and Smurfit Kappa close their merger to form Smurfit Westrock, the new global #1 paper packaging producer at ~$30 billion combined revenue.

October 2024: International Paper announces the acquisition of DS Smith for ~$9.9 billion. Deal closing through 2026 will lift combined revenue near $25 billion.

2025: Stora Enso and Sappi enter a graphic paper partnership to manage European capacity rationalization.

2025: UPM closes the Ettringen paper mill in Germany. Selective graphic-paper exit.

2025-2026: Domtar restructuring: divestiture of select legacy graphic paper assets.

2026: Valmet acquires Severn Group for $480 million. OEM-side consolidation reshaping equipment supply.

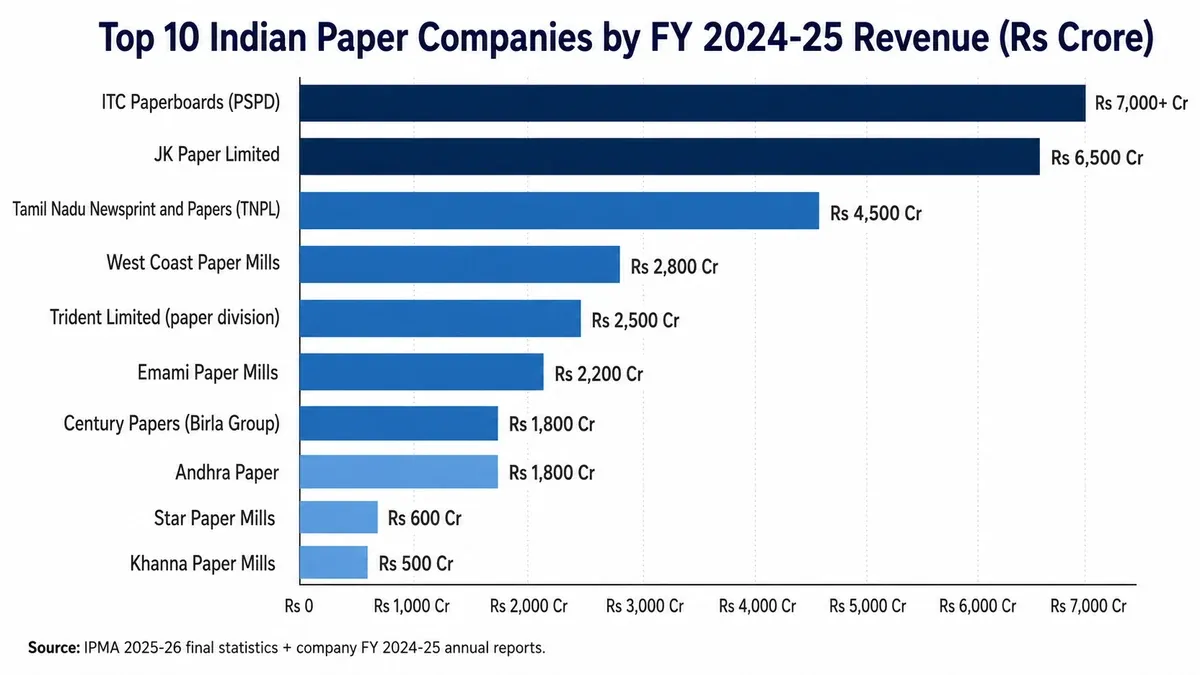

India deserves its own section. With consumption growing 6 to 7 percent annually and Q1 2026 figures trending higher (IPMA 2025-26 statistics and Q1 2026 update) and packaging paper running closer to 8 percent year-on-year, the Indian market is among the fastest-growing globally. The leading domestic producers are a mix of large diversified conglomerates and dedicated paper-focused operators.

Note: Indian company revenue figures are FY 2024-25 (ending March 2025) estimates. Specific values may change with annual report releases and quarterly updates.

Top 10 Indian Paper Companies by FY 2024-25 Revenue: ITC Paperboards Division leads at ₹7,000+ Cr, followed by JK Paper at ₹6,500 Cr. Source: IPMA 2025-26 final statistics + company FY 2024-25 annual reports.

Revenue rank tells one story; product specialization tells another. For buyers, investors, and partners, knowing where each major company places its bets matters:

Packaging leaders: Smurfit Westrock, International Paper, Nine Dragons, Lee & Man, Mondi, Klabin, ITC PSPD

Hardwood pulp export leaders: Suzano, Klabin, CMPC, Asia Pulp & Paper

Revenue rankings can mislead. Pulp-heavy producers like Suzano and Asia Pulp & Paper move enormous tonnage at lower per-tonne prices than premium packaging specialists. By production capacity:

Smurfit Westrock: ~25 million tonnes/year

Nine Dragons Paper: ~20 million tonnes/year

Asia Pulp & Paper: ~19 million tonnes/year

International Paper: ~17 million tonnes/year (post-DS Smith higher)

Suzano: ~12 million tonnes/year (largely pulp)

Lee & Man Paper: ~10 million tonnes/year

UPM-Kymmene: ~10 million tonnes/year

Oji Holdings: ~10 million tonnes/year

Stora Enso: ~9 million tonnes/year

Sappi: ~5 million tonnes/year

Sustainability Profile

Sustainability strategies differ markedly across major producers, but some signals matter for buyers and partners:

FSC chain-of-custody certified: Smurfit Westrock, International Paper, UPM, Stora Enso, Suzano, Sappi, Oji, APP (subset of mills)

PEFC chain-of-custody certified: All top 10 except APP (subset only)

Science-based targets (1.5C aligned): International Paper, Smurfit Westrock, Stora Enso, UPM, Sappi

Carbon-neutral operations target by 2030: Stora Enso, UPM

Carbon-neutral operations target by 2050: Smurfit Westrock, International Paper, Sappi, Suzano, Oji

Market cap and P/E ratio: Public paper companies trade at 8-15x earnings depending on growth profile.

About This Guide

This largest paper manufacturing companies guide is compiled by the World Paper Mill editorial team, a group of pulp and paper industry researchers focused on machinery, capex, and market intelligence for mill operators and project investors. Revenue and production figures are cross-checked against company 2024 annual reports, SEC filings (USA), HKEX disclosures (Hong Kong), Fastmarkets RISI 2025 industry data, AF&PA Q1 2026 outlook, CEPI preliminary statistics February 2026, and IPMA 2025-26 final statistics for Indian companies. Currency conversions use roughly ₹83 per USD (Reserve Bank of India 2026 reference). Private company figures (Asia Pulp & Paper / Sinar Mas) are aggregated industry estimates and may vary from internal reporting.

References & Sources

FAO Forestry Database: 2025 statistical yearbook for global paper and paperboard production.

Fastmarkets RISI: 2025 pulp and paper company financial benchmarks and capacity tracking.

AF&PA: American Forest and Paper Association Q1 2026 industry outlook.

CEPI: Confederation of European Paper Industries preliminary statistics February 2026.

IPMA: Indian Paper Manufacturers Association 2025-26 final statistics.

Company 2024 annual reports: Smurfit Westrock, International Paper, Nine Dragons Paper, UPM, Stora Enso, Suzano, Oji Holdings, Lee & Man, Sappi (publicly available via investor relations pages).

SEC EDGAR (USA), HKEX disclosures (Hong Kong), Tokyo Stock Exchange filings (Japan), B3/Bovespa filings (Brazil).

Industry trade publications: Paper360, Pulp & Paper Canada, Pulpapernews.

Revenue figures are 2024 fiscal-year estimates rounded to one significant figure for comparability. Production capacity numbers combine paper, paperboard, and pulp. INR conversions use roughly ₹83 per USD (RBI 2026 reference). Validate against current company filings and industry reports for transaction-level detail.

Frequently Asked Questions

Smurfit Westrock is currently the largest paper manufacturing company in the world at about $30 billion in 2024 revenue. The company was formed in July 2024 through the merger of WestRock (USA) and Smurfit Kappa (Ireland). The combined entity operates over 500 mills and converting plants across 40+ countries with around 100,000 employees, producing roughly 25 million tonnes of paper packaging annually. Smurfit Westrock surpassed International Paper as the global leader following the merger.

The top 5 paper companies globally by 2024 revenue are: (1) Smurfit Westrock at ~$30 billion (post-2024 merger), (2) International Paper at ~$21 billion (USA), (3) Nine Dragons Paper at ~$11 billion (China/Hong Kong), (4) UPM-Kymmene at ~$10 billion (Finland), and (5) Stora Enso at ~$10 billion (Finland/Sweden). Sources: company 2024 annual reports and Fastmarkets RISI 2025 industry data.

The largest paper manufacturing companies in India by FY 2024-25 revenue are: (1) ITC Paperboards & Specialty Papers Division at ~₹7,000+ Cr, (2) JK Paper Limited at ~₹6,500 Cr, (3) Tamil Nadu Newsprint and Papers (TNPL) at ~₹4,500 Cr, (4) West Coast Paper Mills at ~₹2,800 Cr, and (5) Emami Paper Mills at ~₹2,200 Cr per IPMA 2025-26 final statistics. India is one of the fastest-growing paper markets globally with 6-7 percent annual consumption growth.

The WestRock and Smurfit Kappa merger completed in July 2024 created Smurfit Westrock, now the world's largest paper packaging manufacturer. WestRock (founded 1936, USA) and Smurfit Kappa (founded 1934, Ireland) combined to form an entity with about $30 billion in revenue, 25 million tonnes per year production capacity, 100,000 employees, and 500+ mills and converting plants. The merged company trades on NYSE: SW with dual headquarters in Atlanta, USA and Dublin, Ireland.

Smurfit Westrock leads by production capacity at around 25 million tonnes per year, followed by Nine Dragons Paper (~20 million tonnes, the world's largest containerboard producer), Asia Pulp & Paper / Sinar Mas Group (~19 million tonnes), and International Paper (~17 million tonnes). Capacity rankings differ from revenue rankings because pulp-heavy producers like Suzano and APP move huge tonnage at lower per-tonne prices than premium packaging producers.

Most major paper companies are publicly traded: Smurfit Westrock (NYSE: SW), International Paper (NYSE: IP), Nine Dragons Paper (HKEX: 2689), UPM-Kymmene (HEL: UPM), Stora Enso (HEL: STERV), Suzano (NYSE: SUZ), Oji Holdings (TYO: 3861), Lee & Man Paper (HKEX: 2314), and Sappi (JSE: SAP). Asia Pulp & Paper / Sinar Mas Group is the major exception, held privately within the Indonesian Sinar Mas Group. Most Indian paper companies including JK Paper, TNPL, West Coast Paper, and Andhra Paper trade on the National Stock Exchange of India (NSE).

World Paper Mill's editorial team covers paper manufacturing process, machinery, plant economics, and industry trends. Articles are sourced from industry data and reviewed for technical accuracy.