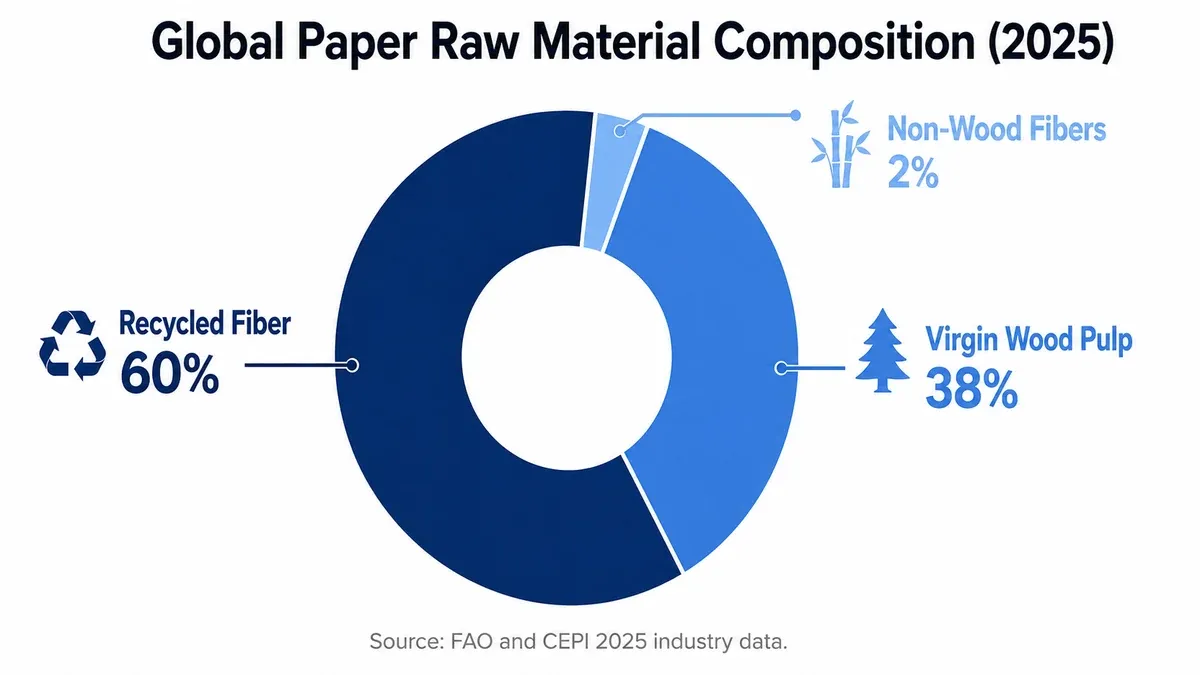

Raw materials for paper industry, also called paper-making raw materials or paper furnish inputs, are the fiber and chemical inputs paper mills use to produce paper, paperboard, and tissue. The three primary fiber sources are virgin wood pulp (softwood and hardwood, about 38 percent of global furnish), recycled fiber (OCC, ONP, SOP, mixed waste, about 60 percent), and non-wood fibers (bagasse, bamboo, wheat straw, kenaf, about 2 percent) per FAO and CEPI 2025 data. Paper mills also use four chemical categories: pulping chemicals (sodium hydroxide, sodium sulfide), bleaching agents (chlorine dioxide, hydrogen peroxide), sizing agents (rosin, AKD, ASA), and fillers (calcium carbonate, kaolin clay, titanium dioxide).

Last updated: 13 May 2026 by the World Paper Mill editorial team. Reviewed against TAPPI, FAO Forestry Database 2025, CEPI 2025, AF&PA 2025, and EN 643 / ISRI PS 2025-2026 data.

Raw Materials for Paper Industry: Quick Reference

Mill operators and project planners can use this table as a quick-scan reference covering 15 raw materials, their category, typical share of furnish, indicative cost band, and primary paper grade applications.

Currency Conversion Reference (approx 2026 spot rates per 1 USD): ₹83 INR (India), €0.93 EUR (Europe), ¥7.20 CNY (China), ¥150 JPY (Japan), £0.79 GBP (UK), CA$1.36 (Canada), AED 3.67 (UAE), BRL 5.10 (Brazil), IDR 15,800 (Indonesia), PKR 280 (Pakistan). Rates indicative; use current spot for transactions. Source: Reserve Bank of India and OANDA composite rates 2026.

Wood Pulp (Primary Fiber Source)

Wood pulp accounts for about 38 percent of global paper furnish in 2025 per FAO Forestry Database (latest published), sourced from managed forests across Brazil, Finland, Sweden, Canada, USA, and Russia. Paper mills blend softwood and hardwood pulp to balance strength against smoothness and cost.

Softwood Pulp (Long Fiber)

Softwood species (Scots pine, spruce, Douglas fir, southern yellow pine) yield long fibers measuring 2.5 to 4.5 mm. Long fibers deliver tensile strength, tear resistance, and ply bonding, making softwood the strength layer in kraft paper, multi-ply paperboard, and packaging grades. Northern bleached softwood kraft (NBSK) is the global benchmark grade.

Hardwood Pulp (Short Fiber)

Hardwood species (eucalyptus, birch, acacia, aspen) yield short fibers measuring 0.8 to 1.5 mm. Short fibers fill voids in the sheet, delivering smoothness, opacity, and bulk for fine paper, writing-printing grades, and tissue. Bleached eucalyptus kraft (BEK) from Brazilian plantations dominates global hardwood pulp export.

Recycled Fiber Grades

Recycled fiber accounts for around 60 percent of global paper furnish in 2025 per CEPI (latest published recycling data). Recovered paper is graded under EN 643 (Europe), ISRI PS (USA), or regional equivalents. Recycled fiber costs 30 to 50 percent less per tonne than virgin pulp but loses fiber strength on each recycling cycle (typically usable for 5 to 7 cycles before disposal).

OCC (Old Corrugated Containers)

OCC is the largest single recycled-fiber grade globally, sourced from used cardboard boxes. It feeds testliner, fluting, and recycled kraft paper production. OCC long-fiber content drives strength in packaging grades. Typical pricing $150 to $350 per tonne depending on grade and region.

ONP (Old Newspaper)

ONP is post-consumer newspaper, processed primarily for newsprint and mid-tier writing-printing grades. ONP requires deinking before high-brightness end uses. Declining newspaper consumption is reducing global ONP supply through 2026.

SOP (Sorted Office Paper)

SOP is high-quality post-consumer office waste paper, typically white grades. SOP processes to fine paper, white tissue, and high-brightness recycled grades after flotation deinking. SOP commands premium pricing among recycled grades at $200 to $450 per tonne.

Mixed Waste Paper

Mixed waste is unsorted post-consumer recovered paper, lowest-cost recycled grade at $80 to $200 per tonne. It feeds low-bright board, fluting, and basic packaging grades. For specifications on each recycled grade, see the complete waste paper grades classification guide.

Non-Wood Fiber Alternatives

Non-wood fibers account for roughly 2 percent of global paper furnish but dominate in regions with limited wood access. India, China, and parts of Latin America operate non-wood-based mills at industrial scale. Non-wood fiber paper carries strong sustainability positioning for premium tissue and packaging brands.

Bagasse (Sugarcane Residue)

Bagasse is the fibrous residue left after sugarcane juice extraction. Indian sugar-belt mills run bagasse at 50 to 90 percent of furnish, producing tissue, writing-printing paper, and food-grade packaging. Annual global bagasse pulp production exceeds 10 million tonnes (FAO non-wood fiber data 2025). Cost is competitive with hardwood pulp at $250 to $400 per tonne (₹20,800 to ₹33,200) in regions with abundant supply (Fastmarkets RISI 2025 non-wood pulp benchmarks).

Bamboo

Bamboo pulp delivers fiber characteristics between softwood and hardwood (1.5 to 2.5 mm). It serves specialty tissue, premium toilet paper, and sustainability-positioned writing-printing grades. China leads global bamboo pulp production. For tissue applications specifically, see the tissue paper manufacturing process guide.

Wheat Straw

Wheat straw and rice straw feed packaging board and fluting in agricultural regions of China, India, and Eastern Europe. Straw fiber length is short (0.8 to 1.2 mm) but adequate for non-strength grades.

Kenaf, Hemp, Cotton Linters

Specialty non-wood fibers for niche applications: kenaf for newsprint substitution trials, hemp for premium specialty paper, and cotton linters for currency paper and high-end art paper. Volume globally is small but pricing premium.

Pulping Chemicals

Pulping chemicals dissolve lignin from wood chips to liberate cellulose fibers. Chemical pulping yields 40 to 50 percent of input wood mass as usable fiber. The two dominant chemistries are kraft (sulfate) pulping and sulfite pulping.

Kraft (Sulfate) Pulping

Kraft pulping uses sodium hydroxide (NaOH) plus sodium sulfide (Na2S), called white liquor, to cook wood chips at 160 to 180 degrees Celsius for 2 to 4 hours. Kraft accounts for near 80 percent of global chemical pulp production (Fastmarkets RISI 2025 pulp benchmarks). The kraft chemical recovery cycle reclaims pulping chemicals from black liquor through a recovery boiler and recausticizing line, making kraft mills largely chemical-self-sufficient.

Sulfite Pulping

Sulfite pulping uses calcium, magnesium, sodium, or ammonium bisulfite to cook wood chips at 130 to 160 degrees Celsius. Sulfite pulping is declining globally in favor of kraft due to chemical recovery and effluent advantages. For a detailed comparison, see the chemical versus mechanical pulping decision guide.

Bleaching Chemicals

Bleaching chemicals raise pulp brightness from natural brown (kraft pulp) or off-white (mechanical pulp) to ISO brightness 60 to 92 percent depending on end-grade target. Modern mills use multi-stage bleaching sequences.

ECF (Elemental Chlorine Free) Bleaching

ECF uses chlorine dioxide (ClO2) as the primary bleaching agent, eliminating elemental chlorine gas (Cl2) which produced dioxin emissions. ECF accounts for ~ 90 percent of global bleached chemical pulp production in 2025 (CEPI and AF&PA 2025 industry data). Typical ClO2 usage 5 to 30 kg per tonne of pulp.

TCF (Totally Chlorine Free) Bleaching

TCF uses oxygen (O2), ozone (O3), hydrogen peroxide (H2O2), and peracetic acid in chlorine-free sequences. TCF commands sustainability premium pricing and is mandated in some European specialty grades. Brightness ceiling slightly lower than ECF but improving with enzyme-assisted bleaching technology.

Sizing Agents

Sizing agents control water and ink absorption in finished paper. Without sizing, ink would bleed and spread on writing and printing grades. Sizing is added either internally at the wet end (most common) or applied to the surface at the size press.

Internal Sizing (Rosin, AKD, ASA)

Rosin sizing (with aluminum sulfate, "alum") is the traditional acid-sizing chemistry, used at pH 4 to 5. Alkyl ketene dimer (AKD) is the dominant modern neutral-sizing agent, used at pH 7 to 8.5, dosing 0.2 to 1.5 percent of furnish. Alkenyl succinic anhydride (ASA) is an alternative neutral sizing agent with faster curing but more sensitive handling requirements.

Surface Sizing (Starch, CMC, PVOH)

Surface sizing applied at the size press uses native or modified starch, carboxymethyl cellulose (CMC), or polyvinyl alcohol (PVOH) to improve printability and surface strength. Starch dosing is typically 2 to 6 percent on paper weight.

Fillers

Fillers improve opacity, brightness, smoothness, and printability while reducing fiber consumption by 8 to 30 percent. Fillers are loaded at the wet end before the headbox. Filler cost per tonne is significantly lower than fiber cost, making filler optimization a key mill economics lever.

Calcium Carbonate (GCC and PCC)

Calcium carbonate is the dominant filler in modern neutral and alkaline papermaking. Ground calcium carbonate (GCC) is mined and ground; precipitated calcium carbonate (PCC) is chemically synthesized for higher brightness and controlled particle morphology. Loading 8 to 30 percent of paper weight depending on grade (TAPPI T440 GSM and filler retention guidelines).

Kaolin Clay

Kaolin clay was historically the dominant paper filler and remains the primary coating pigment for coated grades. Kaolin delivers smoothness and gloss in coatings. Wet end loading 5 to 25 percent for non-coated grades.

Titanium Dioxide (TiO2)

Titanium dioxide is the highest-opacity pigment available, used at 1 to 8 percent of paper weight in premium fine paper, opaque writing-printing, and decorative laminate base paper. TiO2 cost is the highest of any filler at $2,500 to $3,500 per tonne.

Talc

Talc serves as a filler and pitch-control agent in mechanical-pulp grades. Talc absorbs hydrophobic contaminants (wood resins, stickies) from recycled fiber. Loading 2 to 8 percent.

Retention Aids, Strength Resins, and Other Additives

Modern wet-end chemistry uses 5 to 15 functional additives beyond fiber and filler. Each addresses a specific runnability or quality target on the paper machine.

Retention aids: Cationic polyacrylamide (CPAM) and bentonite microparticle systems retain fines and fillers in the sheet rather than losing them through the wire. Dosing 0.05 to 0.3 percent.

Dry-strength resins: Polyacrylamide and cationic starch boost burst, tensile, and ring crush in packaging grades. Dosing 0.2 to 1.0 percent.

Wet-strength resins: Polyamide-epichlorohydrin (PAE) resin provides wet strength for tissue, napkin, and packaging grades that contact moisture. Dosing 0.3 to 1.5 percent.

Optical brightening agents (OBAs): Fluorescent whitening agents that absorb UV and emit visible blue light, raising perceived brightness above 100 ISO. Dosing 0.05 to 0.5 percent for premium fine paper.

For full machine integration of these additives, see the paper production process guide.

Pigments and Coloring Agents

Colored paper grades use direct dyes, basic dyes, acid dyes, or pigments depending on the lightfastness, washfastness, and grade target. Most dyes are added at the wet end before the headbox at 0.05 to 0.5 percent dosing.

Direct dyes: Best fastness on cellulose fiber, used for most colored writing-printing grades.

Basic dyes: High brightness but lower lightfastness, used on mechanical pulp grades where short shelf life is acceptable.

Acid dyes: Reserved for specialty grades with synthetic-fiber content.

Pigments: Insoluble colorants (iron oxide for browns, titanium dioxide for whites, organic pigments for opaque colors) used in specialty board grades.

Raw Material Costs and Sourcing (2026)

Raw materials account for 50 to 70 percent of paper mill operating cost (AF&PA Capital and Energy Report 2025). Cost optimization through furnish blending, recycled-fiber substitution, and filler loading is the largest single profitability lever in mill operations.

Prices indicative for 2026; exact mill economics vary by contract terms, freight, and quality grade. Mill operators planning new investments should reference these bands as starting estimates only and validate with current spot quotes.

Industry Statistics: Paper Raw Material Use Globally

Global paper and paperboard production reached an estimated 410 million tonnes in 2025 per FAO Forestry Database (latest published statistical yearbook). Raw material consumption profile:

- Recovered paper: ~245 million tonnes globally in 2025 per CEPI (~60 percent of furnish)

- Virgin wood pulp: ~155 million tonnes globally in 2025 per FAO (~38 percent of furnish)

- Non-wood pulp: ~10 million tonnes globally in 2025 (~2 percent of furnish, concentrated in India and China per IPMA 2025 and China Paper Association)

- Fillers and additives: ~50 million tonnes globally in 2025 across all categories (estimate per AF&PA and CEPI)

- Bleaching chemicals: ~3 million tonnes ClO2-equivalent globally in 2025 (industry estimate)

Demand drivers reshaping raw material supply chains in 2026 and beyond include packaging growth (e-commerce, food service driving OCC demand), structural decline in graphic paper (reducing ONP supply), and sustainability-driven substitution toward recycled and non-wood sources in premium tissue and packaging across the leading paper producing countries.

About This Guide

This raw materials guide was compiled by the World Paper Mill editorial team, a group of pulp and paper industry researchers focused on machinery, capex, and operations content for mill operators and project investors. Material composition percentages and cost bands are cross-checked against FAO Forestry Database 2025, CEPI sustainability and recycling reports, AF&PA industry statistics, TAPPI technical standards, and EN 643 / ISRI PS recovered-paper grade specifications. We update this guide quarterly to reflect current industry data.

Reviewed: 13 May 2026.

References & Sources

- FAO Forestry Database: Global paper and paperboard production, pulp consumption by fiber source.

- CEPI: Confederation of European Paper Industries recycled fiber utilisation data.

- AF&PA: American Forest and Paper Association industry statistics for North America.

- TAPPI: Technical Association of the Pulp and Paper Industry, fiber and chemical test standards.

- US EPA: ECF and TCF bleaching emissions standards.

- IPMA: Indian Paper Manufacturers Association domestic raw material statistics.

- EN 643 (European recovered paper grade standard) and ISRI PS (Institute of Scrap Recycling Industries paper stock specifications).

All cost bands and percentages are industry-typical ranges for 2026, compiled from Fastmarkets RISI 2026 pulp benchmarks, CEPI 2025 and AF&PA 2025 industry reports, IPMA 2025-2026 price tracking, and manufacturer technical sheets (Andritz, Valmet, Voith Paper, Toscotec, Parason). INR equivalents use approx ₹83 per USD (RBI and OANDA 2026 composite rates). Specific mill economics vary by contract, freight, regional supply-demand balance, and grade quality. Validate against current spot quotes.